NATHANS FAMOUS (NATH)·Q3 2026 Earnings Summary

Nathan's Famous Q3 2026: Revenue Up 9% But Beef Costs Crush Margins Ahead of Smithfield Acquisition

February 5, 2026 · by Fintool AI Agent

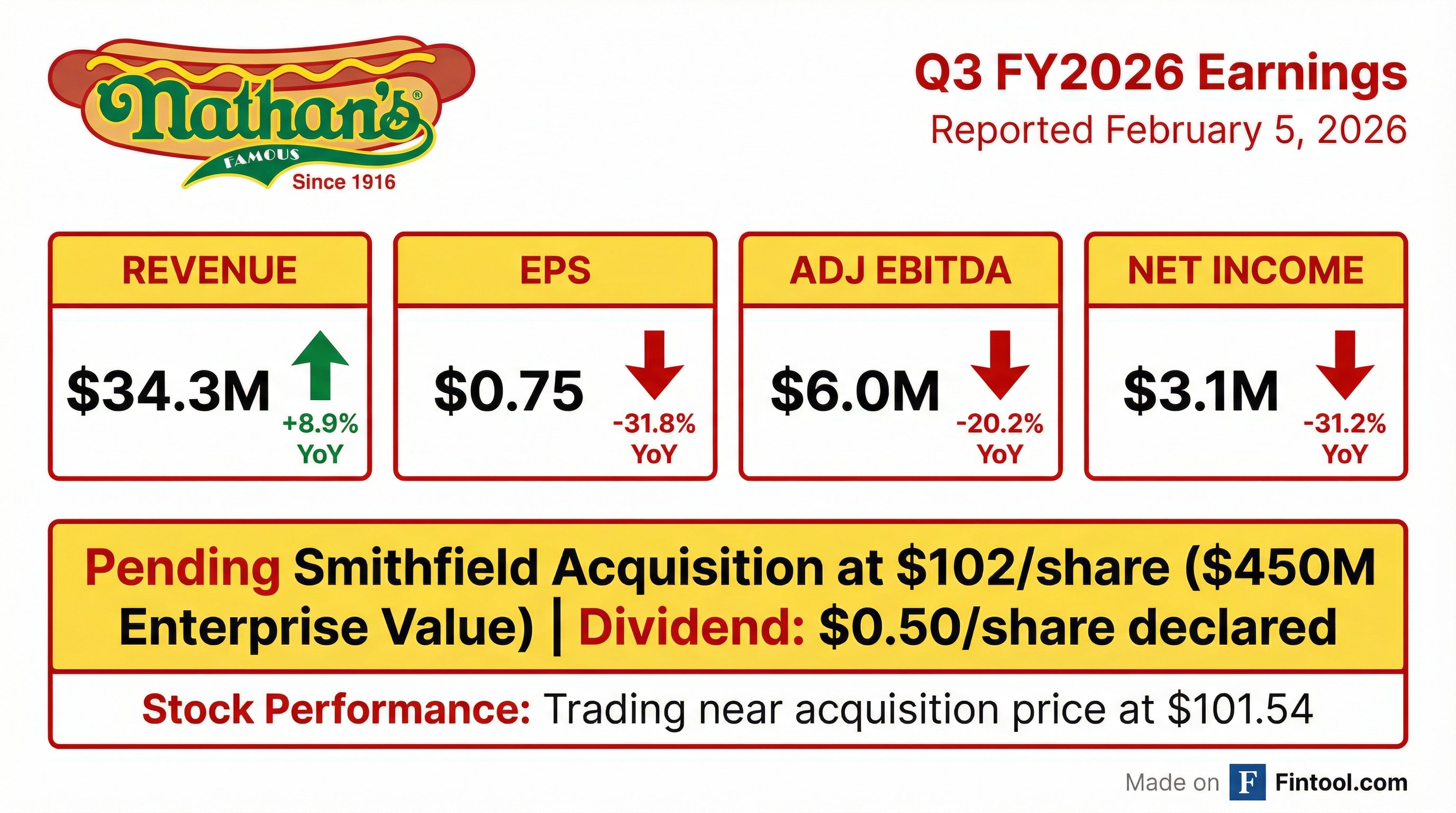

Nathan's Famous reported mixed Q3 FY2026 results on February 5, 2026, with revenue growing 9% year-over-year but profitability taking a significant hit from surging beef costs. The iconic hot dog brand posted EPS of $0.75, down 32% from $1.10 in the prior year quarter, as a 19% increase in beef and beef trimmings costs overwhelmed pricing gains.

The results come amid a pending acquisition by Smithfield Foods at $102 per share, valuing the company at approximately $450 million enterprise value.

Did Nathan's Famous Beat Earnings?

Nathan's Famous has minimal sell-side analyst coverage, so no consensus estimates were available for this quarter. Here's what the company reported versus the prior year:

Key Takeaway: Revenue acceleration was strong, but the margin story was ugly. Operating income fell 24% despite nearly 9% revenue growth, highlighting the severity of cost pressures.

What Changed From Last Quarter?

The Good

- Branded Product Program sales surged 12.6% to $23.7M, driven by 12% higher average selling prices (correlated to beef markets) and 1% volume growth

- License royalties stable at $7.4M (+3.9% YoY), with Smithfield Foods retail program generating $26.3M in YTD royalties

- Franchise operations growing with 18 new locations opened during the fiscal year, despite 23 closures

The Bad

- Branded Product margins collapsed — segment operating income plunged 43% to $1.3M on 19% higher beef costs

- Restaurant traffic down 2% at company-owned locations, partially offset by 1% higher average check

- Net franchise location decline of 5 restaurants during the quarter

How Did the Stock React?

The stock showed minimal reaction, trading near the Smithfield acquisition price:

The stock has been range-bound near $101-102 since the Smithfield acquisition announcement on January 20, 2026. The ~$0.50 discount to the deal price reflects minimal merger arbitrage spread, suggesting high confidence in deal closure.

Segment Performance Deep Dive

Branded Product Program (69% of Revenue)

The Branded Product segment sells Nathan's hot dogs to the foodservice industry. While revenue grew strongly on pricing, margins were crushed by the 19% increase in beef and beef trimmings costs. The company's sales agreements are partially correlated to beef markets, but the pass-through appears insufficient to fully offset input cost inflation.

Product Licensing (22% of Revenue)

The licensing segment remains the crown jewel of the business — essentially pure margin royalty income from Smithfield Foods' retail and foodservice programs. This segment is the primary driver of Nathan's profitability and the key strategic asset Smithfield is acquiring.

Restaurant Operations (8% of Revenue)

Company-owned restaurants continue to struggle with a 2% decline in customer traffic, though average check increased 1%. The segment operates at breakeven to slightly negative margins in the off-peak winter quarter.

Year-to-Date Performance (39 Weeks)

YTD Branded Product Program: Revenue surged 14% to $81.9M, but operating income plunged 55% to $2.5M — the starkest illustration of the beef cost squeeze.

The Smithfield Acquisition

On January 20, 2026, Nathan's announced a definitive agreement to be acquired by Smithfield Foods at $102 per share in cash, for a total enterprise value of approximately $450 million.

Deal Details

- Buyer: Smithfield Foods, Inc. (Nathan's largest licensing partner)

- Price: $102.00 per share, all cash

- Enterprise Value: ~$450 million

- Expected Close: H1 2026

- Conditions: Shareholder approval, HSR clearance, CFIUS approval

Strategic Rationale

Smithfield Foods is already Nathan's largest partner through the licensing agreement, generating $26+ million in annual royalties for Nathan's. The acquisition vertically integrates the Nathan's Famous brand with Smithfield's production capabilities.

Dividend Continues

Despite the pending merger, Nathan's declared its regular quarterly cash dividend of $0.50 per share, payable February 27, 2026 to shareholders of record on February 17, 2026. This is permitted under the merger agreement.

Key Risks and Concerns

-

Beef Cost Volatility: The 19% YoY increase in beef costs significantly pressured margins, and management warned of continued volatility through fiscal 2026.

-

Merger Risk: While the deal appears on track, it requires shareholder approval, HSR clearance, and CFIUS approval. Any regulatory concerns could delay or derail the transaction.

-

Smithfield Dependency: Nathan's licensing revenue is "substantially dependent" on the Smithfield relationship.

-

Labor Inflation: Minimum wage in NYC/Long Island increased to $16.50 in January 2025 and will rise to $17.00 in January 2026, with annual CPI-linked increases thereafter.

Forward Catalysts

Bottom Line

Nathan's Famous delivered a bifurcated quarter — strong revenue growth driven by pricing power, but severe margin compression from beef cost inflation. The Branded Product segment's operating margin collapsed from 10.5% to 5.3% year-over-year, highlighting the company's vulnerability to commodity volatility.

For most investors, the key consideration now is the Smithfield acquisition at $102/share. With the stock trading just below the deal price, shareholders face a simple calculus: collect the dividend and wait for the expected H1 2026 close, or exit now at a modest discount to the acquisition price.

Data sourced from Nathan's Famous 8-K filed February 5, 2026 and company financial statements.